Stablecoin market growth and the US dollar

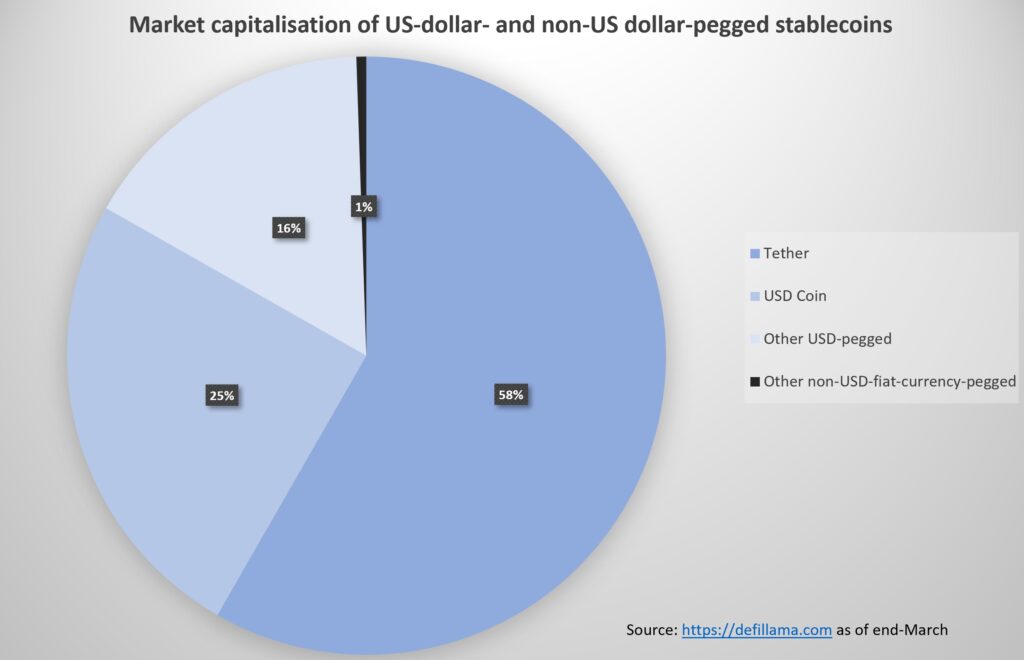

The stablecoin market has grown from USD 5 billion in 2020 to over USD 300 billion in early 2026; it might reach between USD 1 to 3 trillion by 2030, according to Federal Reserve staff. USD‑pegged stablecoins —crypto assets designed to maintain parity with the U.S. dollar — today account for close to 99% of all stablecoin market capitalization (Figure below), with just two names—Tether and USD Coin—capturing the vast majority of that share. This is happening at the same time as geopolitical calls for “de‑dollarization,” rising concern about US fiscal sustainability, and political pressure on the Federal Reserve’s institutional independence. This post asks how these two realities can coexist, and it argues that stablecoins are not eroding the dollar’s exorbitant privilege but are instead creating a digital version of it.

Traditional and digital currency substitution

Traditional finance witnesses a slow, partial diversification away from the USD and there is some high‑profile rhetoric about alternative international payment and settlement arrangements. The European Union has implemented the Markets in Crypto-Assets (MiCA) framework to promote euro-denominated crypto asset alternatives to the USD; China has expanded its digital yuan (e-CNY) pilot programs and explored yuan-backed stablecoins in Hong Kong; and BRICS nations have actively discussed settlement mechanisms outside the dollar system. Nonetheless, digitally, the USD remains extraordinarily dominant, as exemplified by the stablecoin segment.

The dominance of USD-pegged stablecoins cannot be understood through traditional currency substitution theory alone. While classic models emphasize interest rate differentials, inflation expectations, and transaction costs, digital currency markets exhibit distinct properties that amplify the advantages of certain currencies along at least three dimensions.

Common knowledge

First, Berg et al. (2024) describe dollar dominance in stablecoin markets as rooted in the recursive belief that “I know what a dollar is worth, I know that you know what a dollar is worth, and you know that I know that you know what a dollar is worth.” A USD‑pegged stablecoin can “free‑ride” on decades of accumulated understanding of the dollar’s value, both in the United States and abroad. Euro or yuan stablecoins, by contrast, must build such common knowledge from a negligible base in the crypto ecosystem, even if those currencies are well‑known in traditional finance.

Network effects and path dependence

Second, digital infrastructures make it trivial to express that preference. In earlier work on pegged crypto assets, I argued that stablecoins aim to function as digital anchors linking crypto markets to fiat monetary systems, although their empirical performance in this regard is not impressive. Be that as it may, the anchor role turns out to be highly asymmetric: USD‑pegged instruments provide a focal numéraire in decentralized finance, in centralized crypto exchange markets, and in cross‑border transfer use cases. This focal position is reinforced by network effects and path dependence.

Stablecoins reshape the “impossible trinity”

Third, the “impossible trinity” of international finance—wherein countries cannot simultaneously maintain independent monetary policy, stable exchange rates, and open capital accounts—takes on new dimensions with stablecoins. Benigno et al. (2022) show that in a two-country framework with global stablecoins, interest rates tend to synchronize across countries, making users increasingly indifferent between holding domestic currency and the stablecoin. In such an environment, the incumbent reserve currency’s advantages—liquidity, collateral usefulness, and depth of financial markets—are not diluted by digitalization; they are scaled. Digital rails do not level the playing field; they tilt it further toward the US dollar.

Emerging market hedging and welfare

The demand side of “crypto dollarization” is driven in large part by emerging market economies. For households facing persistent inflation, currency depreciation, and financial repression, dollar‑denominated digital assets are a natural hedging vehicle.

Murakami and Viswanath‑Natraj (2025) show that in countries like Turkey and Argentina, stablecoins can improve household welfare by providing a more stable savings instrument and smoothing consumption in the face of macroeconomic shocks. Both banked and unbanked households benefit, with stablecoins acting as a low‑friction channel into dollar assets that bypass traditional banking constraints. Ahmed et al. find that crypto adoption responds to sovereign risk: higher CDS spreads are associated with more crypto‑app downloads and usage, which is consistent with households turning to digital assets as a way of hedging default and inflation risk. Ahmed et al.’s (2024) find that crypto adoption responds to sovereign risk: higher CDS spreads are associated with more crypto‑app downloads and usage, which is consistent with households turning to digital assets as a way of hedging default and inflation risk.

Financial subordination

At the same time, a literature on international financial subordination emphasizes that greater access to foreign‑currency instruments can deepen structural dependence. Perfeito da Silva and Zucker‑Marques (2025) argue that fintech tools that ease access to foreign currency and crypto can accelerate capital outflows and intensify dollarization. Evidence from stablecoin transaction flows suggests that emerging market currencies with stronger Tether usage are also characterized by higher exchange‑rate volatility. This can create a self‑reinforcing dynamic: domestic instability drives stablecoin adoption; that adoption puts further pressure on the local currency and reduces room for domestic policy.

There is no contradiction between the views on financial subordination on the one hand and emerging market hedging and welfare on the other. From the standpoint of individual households, digital dollarization can be welfare‑enhancing. From the standpoint of macro‑level monetary sovereignty, it can erode autonomy and deepen financial subordination. Stablecoins make this tension more acute, and this assessment is consistent with research discussed in an insightful recent blog post.

Regulation as amplifier

On the supply side, the stablecoin market is highly concentrated. A small number of US dollar‑pegged issuers dominate, benefiting from strong network effects, established liquidity, and integration into major trading venues. Empirically, episodes of severe market stress—such as the Terra/Luna collapse or the Silicon Valley Bank episode—have hit the major US-pegged stablecoins less (even though Tether temporarily lost its peg) than other stablecoin designs such as crypto-backed or algorithmic ones.

Regulation has tended to reinforce this pattern. The US GENIUS Act (and related initiatives) establish a unified framework for dollar‑pegged stablecoins, requiring full backing in short‑term Treasuries or dollars and regular reserve disclosures. This provides legal clarity and supervision for the largest USD issuers — that is Tether, followed at a distance by USD Coin — making them even more attractive as infrastructure for international payments and settlement arrangements. Crucially, it was accompanied by the CBDC Anti-Surveillance State Act that prohibits the Federal Reserve from issuing a retail central bank digital currency (CBDC), thus barring a state-issued competitor to private issuers of US-dollar pegged stablecoins.

Here the strategic dimension becomes visible. US policymakers have openly discussed the potential for stablecoins to generate large additional demand for Treasury bills and bonds, likening this to a new “global saving glut”. In my reading, this is not merely an accidental by‑product of regulation: it seems that US regulators are consciously trying to entrench the “digital exorbitant privilege” by encouraging regulated, US-dollar‑backed stablecoins that sit squarely inside the US legal and financial perimeter. Stablecoin regulation becomes, in part, an instrument of public debt management.

The digital exorbitant privilege

Taken together, these pieces help resolve the paradox. On‑chain, we see:

- a massive initial advantage due to the dollar’s common‑knowledge status,

- strong network effects and issuer concentration in USD‑pegged coins,

- structural EM demand for dollar hedges via digital channels, and

- regulatory choices that backstop dollar‑linked designs.

This configuration does not weaken the dollar’s exorbitant privilege; it extends it into a new technological layer. Stablecoins generate additional demand for US securities, embed the dollar more deeply into DeFi and cross‑border retail usage, and give US authorities new levers of influence (and surveillance) over flows transiting through dollar‑linked chains. Even if traditional metrics—such as the dollar’s share in official reserves—show gradual diversification, the rapid growth of stablecoins ensures that the dollar remains the dominant unit of account in this fast‑growing segment of global finance.

Within the broader monetary system, stablecoins may still be subsidiary in scale. But within their own domain, they exhibit “winner‑take‑most” dynamics that lock in incumbents. Absent structural disruptions — such as a serious erosion of US institutional monetary credibility –developments in this domain are likely to reinforce, not erode, the US dollar’s international role.

That is what I call in reference to Giscard d’Estaing’s original concept “exorbitant privilege 2.0”: a digital extension of US monetary power, emerging as a result of the way crypto asset markets are evolving. Stablecoins create new demand for Treasuries, extend dollar hegemony into decentralized finance ecosystems, and provide mechanisms for sanctions enforcement through blockchain surveillance.